Research

Working Papers

Language Frictions in Consumer Credit [SSRN] [Slides]

Abstract

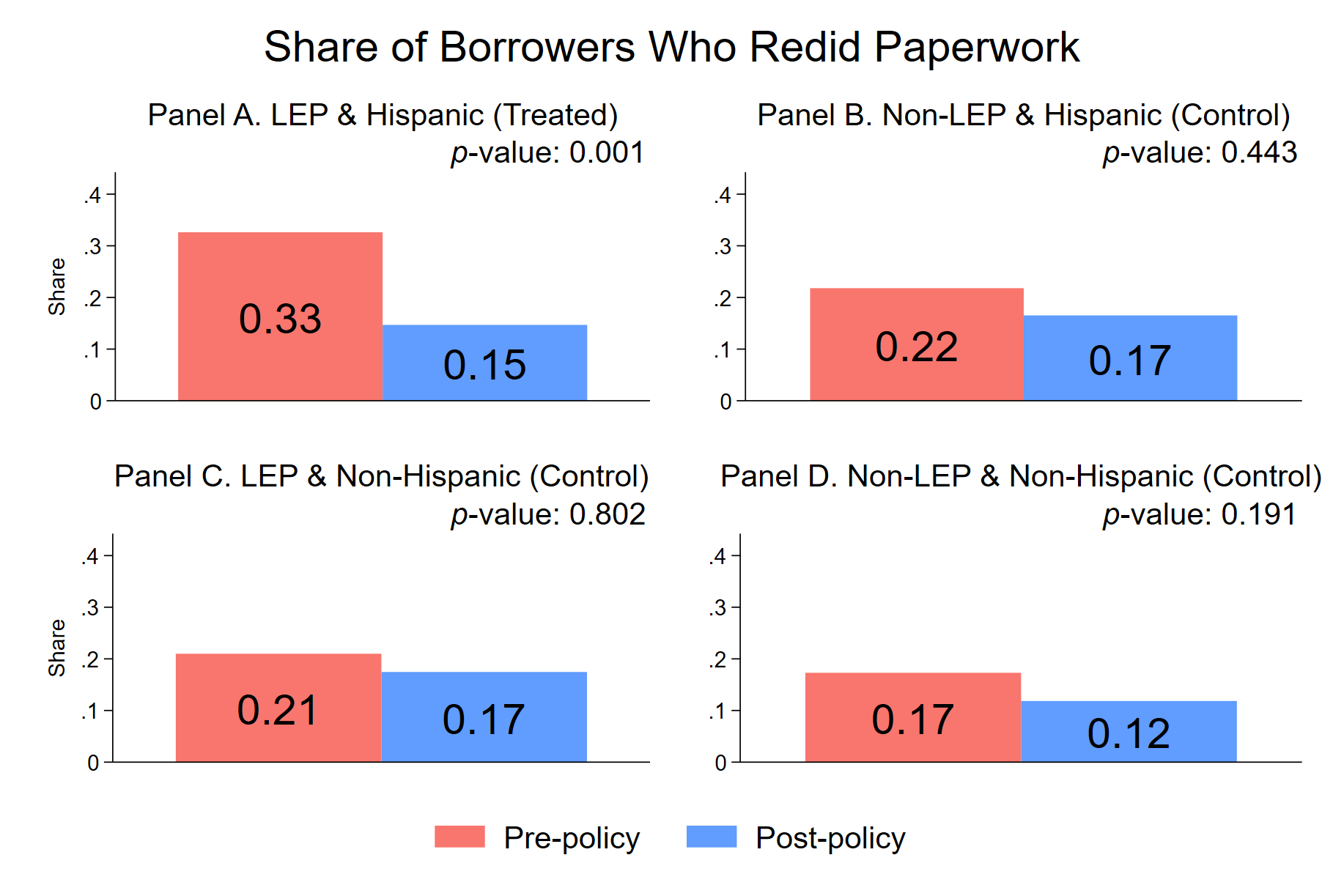

This paper studies how language barriers between lenders and borrowers translate into differences in borrower outcomes in the U.S. mortgage market. I use survey data to infer and machine learning techniques to predict borrowers' English proficiency. I document significant descriptive differences in perceptions of mortgages, application experiences, and mortgage rates between limited English proficient (LEP) and non-LEP borrowers. To measure the causal effects of language frictions, I exploit a Federal Housing Finance Agency policy that provided translated mortgage documents in Spanish to mortgage lenders. After the policy change, LEP Hispanic borrowers had a streamlined application process, contacted more lenders, understood mortgage contracts better, and enjoyed lower borrowing costs. Reducing language frictions also led to expanded access to credit for LEP borrowers. Overall, my findings highlight a cost-effective way to create a responsible inclusion of well-qualified LEP borrowers in the mortgage market.

Income Inequality, House Prices, and Housing Regulations [SSRN] [Slides]

with Edmund Y. Lou and Wei Xiang

Abstract

This paper studies the relationship between income inequality and house prices in the United States. We exploit the initial income distribution across 90 occupation-income percentile groups and the national income growth of these groups to construct instruments for income inequality measures, effectively addressing reverse causality concerns. Using county-level data from 1990 to 2017, we find that a one standard deviation increase in the Gini coefficient leads to a 26% increase in house prices. We propose a supply-side channel to explain the observed higher prices and fewer housing stocks in more unequal areas. Consistent with this mechanism, our analysis shows that a one standard deviation increase in the Gini coefficient results in an increase in the 2018 Wharton Residential Land Use Regulation Index by 0.35 standard deviations, leading to 14% fewer housing units, 58% fewer building permits over the next decade, and a 2 percentage point decrease in homeownership rate. Our findings highlight the importance of income inequality in shaping housing market dynamics through its impact on housing regulations and the consequences for housing affordability.

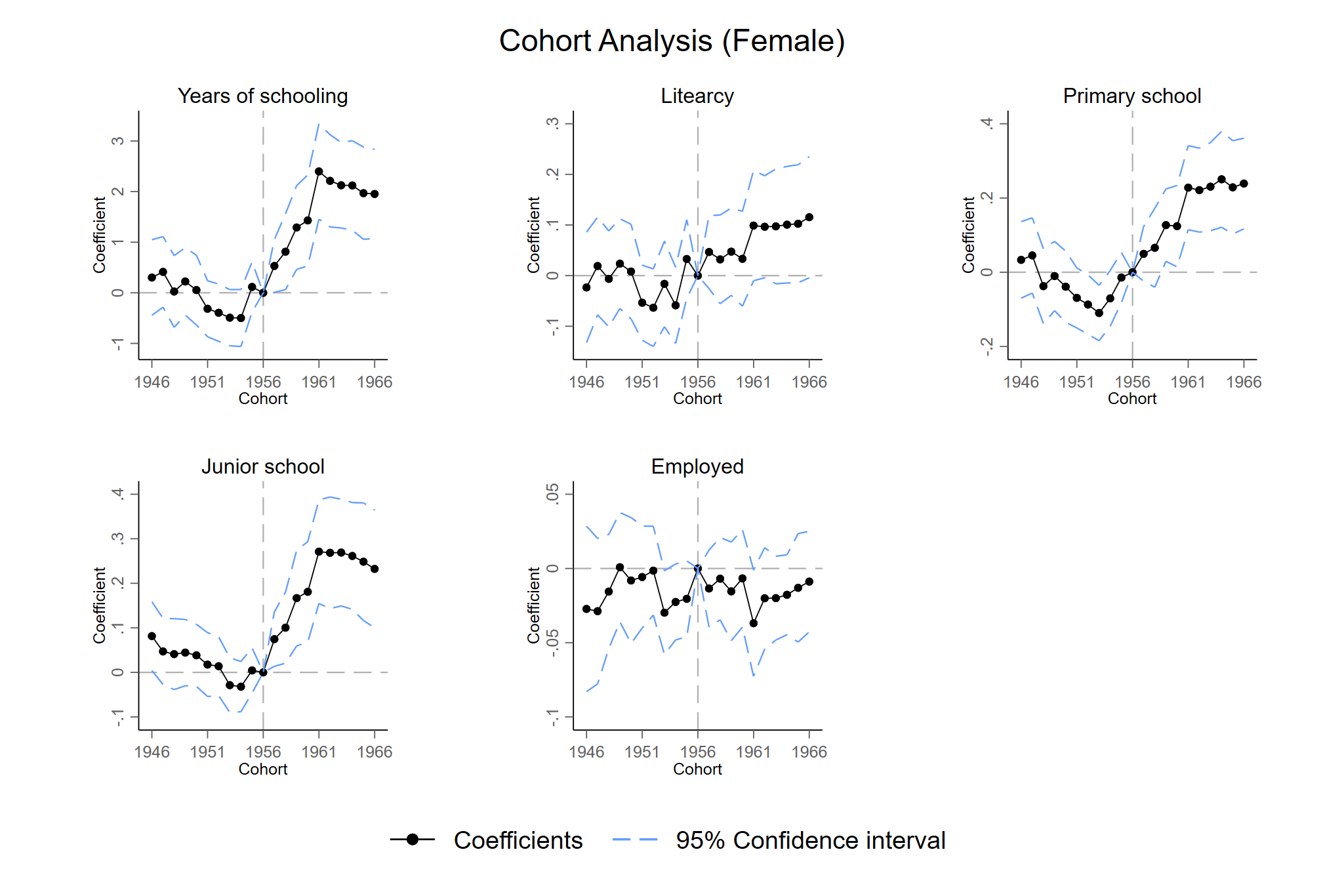

The Very Long-Run Effect of Large-Scale Deworming in China [SSRN] [Slides]

with Gordon G. Liu

Abstract

This paper studies the long-term impacts of an unprecedented large-scale schistosomiasis control campaign in China in the late 1950s. We present one of the first direct evidence of how an early-life deworming intervention affected life trajectories. The deworming program had a positive effect on the educational attainment of rural people. The effect was larger for people from a low socioeconomic background, suggesting that the program reduced educational inequality. Early-life exposure to the program had substantial effects on labor market success and economic status 50 years later, as well as on the second generation's schooling.

Selected Work in Progress

Quantifying the Effect of Mortgage Broker Licensing Regulations

with Tianshi Mu

Regulating Asset Resales: Evidence from Taiwan’s Housing Market

with Shi Gu and Edmund Y. Lou

Liability Systems and Innovation: Evidence from 19th Century England

with Jinlin Wei